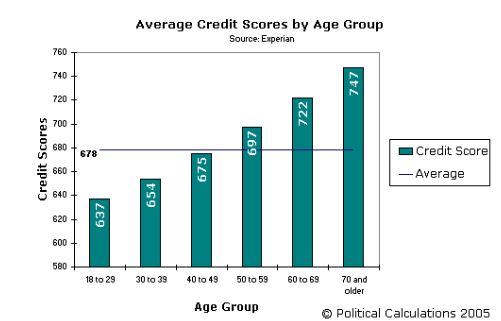

Overall, the average credit score is decreasing over time, especially for the younger age groups. So it only makes sense that people would be concerned about negative information on their credit reports, and how long it will stay there. Read on to find out how the negative things on your credit report might impact your financial health in the long term.

The unfortunate truth is that many negative financial decisions can, and will, stay on your credit report for years. But don’t lose hope! There are ways to rebound from this. Luckily, the older negative marks on your credit are, the less weight they carry. That means that if you made a financial mistake recently, it would hurt you the most now. And a few years down the line, while it will still be there, it will be considered less important. This works both ways, positive aspects of your credit report will stay there infinitely as well.

The bottom line

Negative information, like as late payments, are erased after seven years on your credit report. A charge-off, or an account you did not pay as agreed, will also stay there for up to 7 years. This includes credit cards that have been charged off, and also loan balances. Many of these debts get sold off to collectors, and that is when it goes on your report. So it’s important to avoid your debt going to collections at all costs.

A foreclosure also stays on your report for seven years. This can impact your interest rates on future loans, and your ability to qualify for a new mortgage. It will often read as settled for less than the amount due on the credit report.

Inquiries and your Credit Report

Inquiries will sometimes affect your credit score and go on your report. However, there are two different types of investigations: hard and soft. The baseline is that soft inquiries do not change your credit score, and hard ones do. But how do you tell the difference?

A soft inquiry can be one of many things. Usually, it is a credit check you perform on yourself. In other words, you go online and get a report on your credit history to check up on things and look for mistakes. This does not affect your credit. It does appear on your statement, but it does not change your credit score or anything else.

A hard inquiry is conducted by someone else. Most often, this happens when you apply for a new loan, credit card account, or mortgage. It will slightly decrease your credit score, probably to discourage people from applying for a million credit cards at once. The hard inquiry stays on your credit report for two years. After that, it stops affecting anything. Hard inquiries don’t change anything about your credit after a year, even though they will remain on your report.

Special Cases in New York and California

In some states, additional rules apply. For example, one of the rules in New York is that accounts that go to a collection agency and then are paid only stay on your report for five years, not seven. Satisfied judgments will be on your credit report for seven years after they are released (or alternately ten years after the date they were filed).

The same goes for unpaid tax liens. All of the others rules stated above apply.

What about public records?

Some public records also go on your credit report and stay there for a while. Bankruptcies are always removed seven years after the release date, or ten years after the filing date.

Surprisingly, an eviction itself will not go on your report. But, financial lines tied up with the removal definitely do. It is likely that your landlord might have sent the unpaid rent to a debt collector, in which case it will show up on your report for seven years.

What can I do to improve my credit score with negative marks?

Fortunately, there are many ways to improve your score in the meantime before the negative remarks are removed from the report:

- Setup payment reminders so you don’t keep missing payments

- Improve your debt-to-credit ratio by paying off debts, especially revolving debts

- Make sure you are not spending more than you make

- Keep close watch on your credit report for any changes

- Come up with a payment plan that will let you spend your budget on essentials, paying off your debt, and enough left over for a little leisure.

Leave A Comment