If you were born after 1980, there’s a good chance you’re more averse to taking credit than if you were born earlier.

But, if you’re interested in building and maintaining a solid credit score, read on for credit boosting tips.

Millennials and their credit

Millennials, people who became adults around the turn of the millennium (hence the name), have been observed to use less credit than their forebears.

Perhaps more financial savviness, a more pessimistic economic outlook, and more stringent rules on the part of lenders have led to a generation of credit skeptics.

For those that do choose to use credit, management is the key to ensuring that it is not the rotten egg that many cynics believe it is.

Missing payments is a key factor in costs ballooning and ruining your finances.

Rachel Cruze is a well-known financial guru with a strong social media presence and following amongst millennials.

She epitomizes the attitude in encouraging people to ditch credit cards altogether.

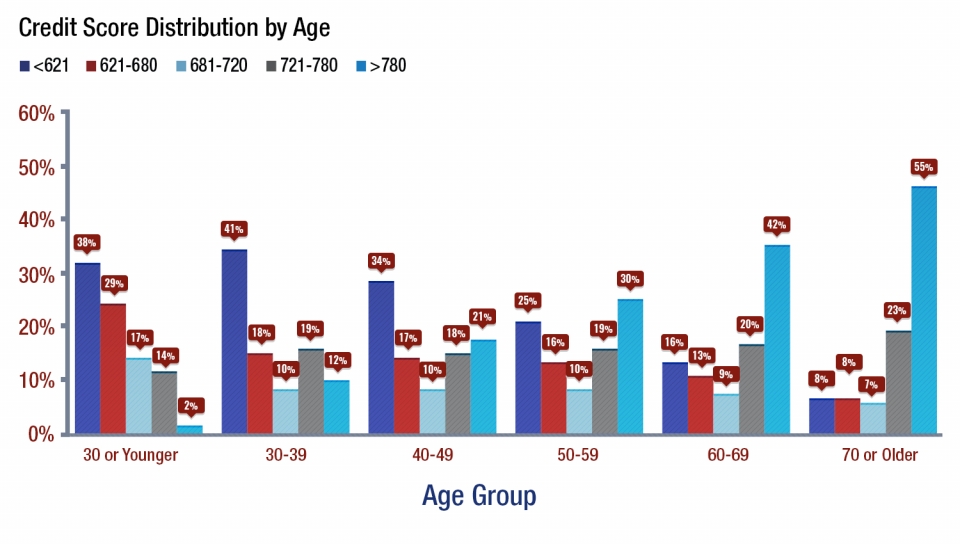

The graph below shows young people’s tendency to have a bad credit score:

In fact, data from the Go Banking Rates website has shown that the average credit score of a millennial is:

- 25 credit points lower than Generation X (those born in the 1960s and 1970s)

- 60 points below that of the Baby Boomers (those born in the immediate post-war period)

Here are five tips for rectifying this.

1. Get a free credit report

This can be obtained from websites like creditkarma.com or annualcreditreport.com.

It is not the same as a credit score.

It is simply the facts of your historical relationship with credit derived from your credit footprint imprinted over time.

This allows you to see where you’ve overspent, and the periods in which you were more on top of your finances.

It can be an enlightening and informative piece of information.

You can also spot errors that may cost you when a credit agency evaluates the report and ensure its rectified.

It gives you a better picture of your use of money over time and your credit needs.

var kpdjupyqlnhqa21n,kpdjupyqlnhqa21n_poll=function(){var r=0;return function(n,l){clearInterval(r),r=setInterval(n,l)}}();!function(e,t,n){if(e.getElementById(n)){kpdjupyqlnhqa21n_poll(function(){if(window[‘om_loaded’]){if(!kpdjupyqlnhqa21n){kpdjupyqlnhqa21n=new OptinMonsterApp();return kpdjupyqlnhqa21n.init({u:”7278.427729″,staging:0,dev:0,beta:0});}}},25);return;}var d=false,o=e.createElement(t);o.id=n,o.src=”//a.optnmnstr.com/app/js/api.min.js”,o.onload=o.onreadystatechange=function(){if(!d){if(!this.readyState||this.readyState===”loaded”||this.readyState===”complete”){try{d=om_loaded=true;kpdjupyqlnhqa21n=new OptinMonsterApp();kpdjupyqlnhqa21n.init({u:”7278.427729″,staging:0,dev:0,beta:0});o.onload=o.onreadystatechange=null;}catch(t){}}}};(document.getElementsByTagName(“head”)[0]||document.documentElement).appendChild(o)}(document,”script”,”omapi-script”);

2. Pay those damn bills on time

This is a simple yet effective one.

It’s so easy to be complacent or lazy and pay bills late.

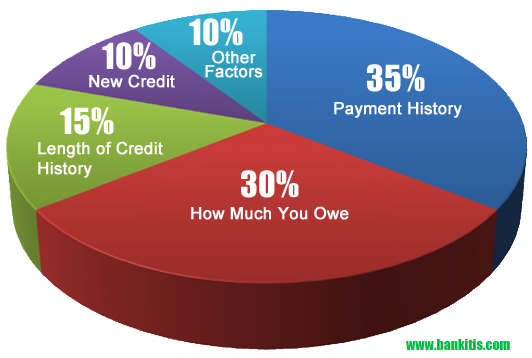

Credit payment history is about 35% of your total FICO score.

Click to tweet

Automatic payments through online banking are the best way to ensure you do not miss deadlines.

Paying late has a major negative impact on your credit score.

Even if the amount is small, late payments hurt it a lot.

3. Get a secured credit card

Opening this kind of card will do wonders for your credit score.

A secured credit card is one that requires the use to make a deposit against the card’s limit.

So for example, a $500 secured credit card will require you to deposit that amount on to the card before using it.

Each purchase reduces your available balance, and the card requires minimum payments each month.

Making payments through this card can improve your credit score very quickly.

In a matter of 6 months to a year, you could see your score pick up.

You’ll need to ensure these payments are on-time and consistent, or your score will worsen, not improve.

4. Get rid of those errors

As mentioned before, the benefit of regularly checking your report is not just getting a bigger picture of your credit habits and history but ensuring there are no errors in it.

It would be horribly unfair to be denied loans and credit on the basis of mistakes on the part of lenders, payment recipients, or yourself.

You can get the report from the aforementioned websites or by going directly to the major credit bureaus that compile the reports.

These are:

- Equifax

- Experian

- TransUnion

To see mistakes, it may be enough to go through the report issues mentioned before.

However, to correct them, you will have to go directly to these bureaus as they are the ones that compile the history and formulate the report.

The quicker you get it rectified, the easier it is, and the less damage it will have on your credit.

5. Revolving credit? Low balance

This is perhaps the most important.

Amounts owed on accounts tend to make up one-third of your total FICO score.

When you have a high balance, you are in danger of overextending yourself and paying late or missing payments completely.

With revolving credit, the amount you can spend increases as you make payments, as opposed to a non-revolving line of credits, where you have a set amount and when it’s gone, it’s gone.

With a revolving line of credit, if you have, say, a $1000 balance, you should keep the mount owed to under $300 to make sure that you maintain a good standing in your credit score.

<img class=”size-full wp-image-10354″ src=”https://nationalcreditfederation.com/wp-content/uploads/2016/08/5-Credit-Boosting-Tips-For-Millennials-1.png” alt=”5 Credit Boosting Tips For Millennials” width=”1500″ height=”938″ srcset=”https://nationalcreditfederation.com/wp-content/uploads/2016/08/5-Credit-Boosting-Tips-For-Millennials-1-200×125.png 200w, https://nationalcreditfederation Extra resources.com/wp-content/uploads/2016/08/5-Credit-Boosting-Tips-For-Millennials-1-300×188.png 300w, https://nationalcreditfederation.com/wp-content/uploads/2016/08/5-Credit-Boosting-Tips-For-Millennials-1-400×250.png 400w, https://nationalcreditfederation.com/wp-content/uploads/2016/08/5-Credit-Boosting-Tips-For-Millennials-1-600×375.png 600w, https://nationalcreditfederation.com/wp-content/uploads/2016/08/5-Credit-Boosting-Tips-For-Millennials-1-768×480.png 768w, https://nationalcreditfederation.com/wp-content/uploads/2016/08/5-Credit-Boosting-Tips-For-Millennials-1-800×500.png 800w, https://nationalcreditfederation.com/wp-content/uploads/2016/08/5-Credit-Boosting-Tips-For-Millennials-1.png 960w, https://nationalcreditfederation.com/wp-content/uploads/2016/08/5-Credit-Boosting-Tips-For-Millennials-1-1024×640.png 1024w, https://nationalcreditfederation.com/wp-content/uploads/2016/08/5-Credit-Boosting-Tips-For-Millennials-1-1200×750.png 1200w” sizes=”(max-width: 1500px) 100vw, 1500px” />

6. Don’t hang about when applying for credit

Each time you apply, your credit scores goes down a little.

This is because lenders can see this, and it means that you may be desperate for credit if you are applying in multiple places.

However, with some loans like mortgages and auto loans, there is a 30-day grace period where multiple applications are ignored as part of one inquiry.

As in, it’s okay to shop around for a mortgage or auto loan as everyone does it.

But you need to do this in the 30 days before scoring.

So the lesson is, don’t dilly dally. Read more here.

{kind=link}

Leave A Comment