Have you missed a couple of payments? Are you worried that these late payments may have ruined your credit score?

Don’t freak out just yet!

Here’s how payment history affects your FICO score, and what you can do about it.

What is my FICO score and why does it matter?

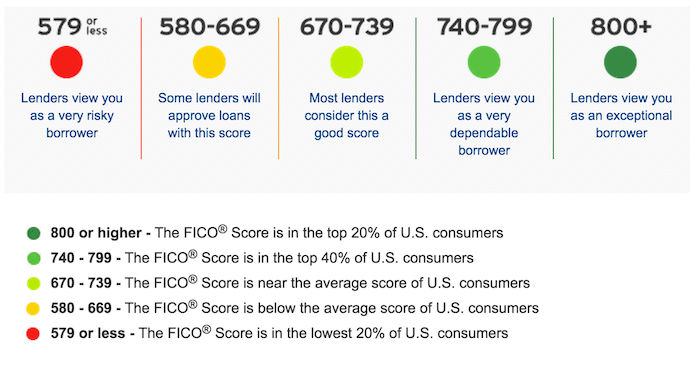

Your FICO score is a number between 300 and 850, which gives financial institutions and lenders a clear picture of the risk they would take in lending you money.

The higher the number, the better your score.

In the US it is used by:

• All of the Top 50 financial organizations

• The 25 major credit card issuers

• The 25 major auto lenders

• A wide range of other businesses

How is it calculated?

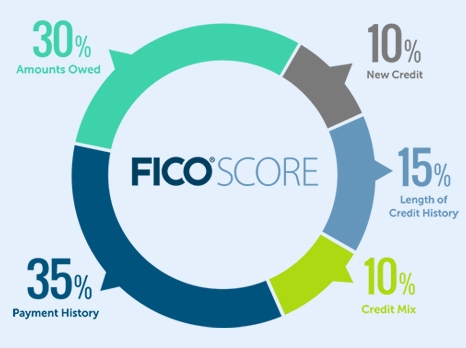

The actual algorithm used in calculating your score is a closely-guarded secret.

However, on their website, FICO does explain all of the factors that they include and the weight each of them receives.

As you can see, the most influential factor in your FICO score is your payment history.

This makes up 35% of your credit score.

But what does that include, and how can you make it work for you?

What influences my payment history?

There are a number of factors that make up your payment history:

- Current Status

- Prior Late Payments

- Narrative Codes

- Collection items

- Accounts with NO LATE PAYMENTS

These apply to several account types; credit cards, store accounts, installment loans – e.g. auto or student loans – mortgage loans and finance company accounts.

Lenders report back to the credit reporting agencies about all activity on these types of accounts, and the data from these reports is fed into the calculation algorithm.

Let’s look at each of the factors of your payment history in greater depth:

1. Current status

In a lender report, a system of numeric codes is used to show the payment status of your account.

A status of 1 means that the account is being paid as agreed, and a status of 2 shows that the account is up to 30 days past due.

The codes continue up to 9, with successive numbers being linked to greater degrees of delinquency on the account.

Ideally, you want each of your account reports to show a number 1 – this means that you are up to date with your payments which will ultimately lead to a better score.

2. Previous late payments

Your report will also show a history of the payments on each of your accounts.

By federal law (The Fair Credit Reporting Act), negative payment information will remain on your credit report for up to seven years (and up to 10 for bankruptcies).

So any missed payments will affect your credit score for that length of time.

This is still the case, even if you catch up with payments and the lender marks the account as current.

3. Narrative codes

Narrative codes are the descriptors applied to your account as part of the lender’s report. They can be neutral or negative, and a negative code (such as ‘Repossession,’ ‘Foreclosure Process Started’ or ‘Settlement accepted on this account’) can have a major, long-lasting effect on your credit report and FICO score.

4. Collection items and matters of public record

Collection occurs when lenders sell a past-due account to a collection agency which specializes in collecting consumer debts.

Such companies will receive a fee from the lender once they have collected part or all of the debt.

Matters of public record that would appear on your credit report are bankruptcies, tax liens, and judgments.

These are collected from courthouses, verified by public record vendors, and then added to your report.

Both public records and collections will have a significant negative impact on your FICO score.

5. Accounts with no late payments

Accounts with NO late payments are IDEAL.

If these make up the majority of the accounts mentioned in your credit report, then this will have a very positive effect on your FICO score.

Don’t panic if not all of your accounts are in this state, though; as FICO explain, “A few late payments are not an automatic “score-killer.” What is most important is an “overall good credit picture.”

Improving your situation

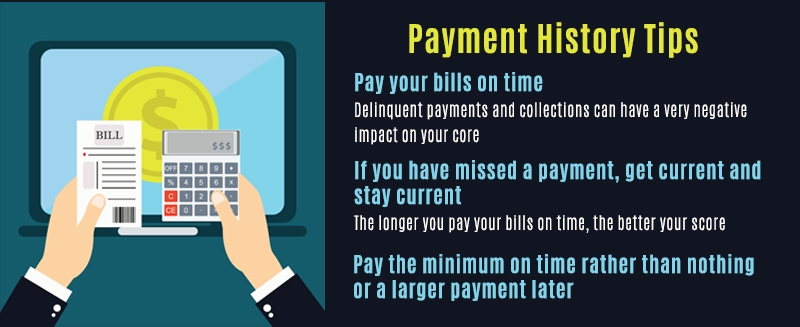

Your payment history is the most significantly weighted aspect of your FICO score. It is also the one you have the most control over.

By making sure that you make every payment on time, you can really have a significant, positive effect on your score.

Even if there are missed payments or other problems in your financial past, making good choices now can help you to start improving your score.

Leave A Comment