For first-time house hunters, buying a home can be challenging.

They’ll need to determine the location, style, size, and price range of the potential home.

In addition to that, they’ll need to consider the different mortgage options, and figure out how much of a down payment they can afford.

Bank Loans Needed for Homebuyers

All bank loans have interest rates and fees.

These must be paid in addition to paying off the value of the loan.

Interest rates vary depending on the type of loan.

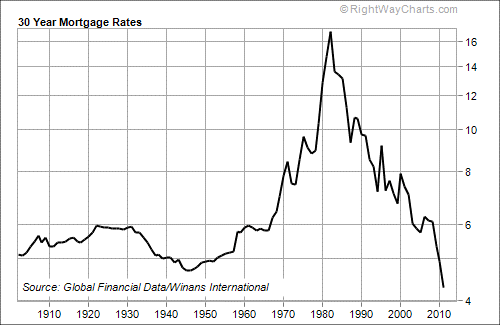

Currently, for mortgages, interest rates in America range from 2.65% to 3.75%.

The exact rate depends on the location and the issuing bank.

If you are looking at buying a home, a mortgage is the type of loan that will help you get the home of your dreams.

Loans are not guaranteed, but there are a few things that will help you secure your financing.

Having a continuous job, reliable income, and a reasonable credit score will make your file more favorable to lenders.

How Your Credit Affects Your Mortgage

Credit scores are dependent on the payment of debt, be it credit cards, loans, or lines of credit.

Scores are lower for users who miss or make late payments.

To have a good credit score, one must acquire debt and then continue to pay it off on time.

A good credit score is generally over 620, and if the score is over 720, it is considered excellent.

For banks, a score over 700 or so is an easy acceptance.

The Basics of Having a Mortgage

There are two different rate options for mortgages: fixed or adjustable.

Fixed rates will have the same interest rates over the span of the term, meaning that the monthly payment is reasonably constant.

Adjustable rates may start lower, but after a few years, the rate will change based on the market interest rates.

If particulars of the owner’s life change, they can refinance their home.

Doing so involves paying off the original mortgage and signing a new one.

When refinancing, the interest rate, the length of the mortgage, and the type of rate can change.

Start Your Life as a Home Owner with a Down Payment

In addition to having a mortgage, homeowners will need to put a down payment on their new home.

The down payment amount is deducted from the value of the mortgage.

Usually, the down payment is 20% of the value of the home.

Some Loans to Consider for First-Time Home buyer

Some banks and lenders offer loans with smaller down payments.

For eligible buyers, the down payment may be as low as 3%.

A lower down payment means that the new owner will have more savings for emergencies and repairs.

- A classical loan is one from the FHA (Federal Housing Administration). One type of FHA loan is the 203(b), which is insured by the government. For those with a credit score above 580, the down payment is 3.5%. If the credit score is between 500 and 579, the down payment is 10%.

- Freddie Mac issues a Home Possible Mortgage. The down payment rate is between 3 and 5%. However, the mortgage must be for the owner’s primary and sole residence. Additionally, their income must be at or below the area median income, with two exceptions. The loans have a maximum term of 30 years for fixed rate and adjustable rate loans.

- Fannie Mae has a loan called the Conventional 97. This is designed for single-family homes and first-time homeowners. There is no income limit, but homebuyers must complete an education program. The Conventional 97 has a 3% down payment rate for loans less than $417,000.

- Fannie Mae offers a second loan called HomeReady. This loan also has a 3% down payment rate. The owner doesn’t need to be a first-time home buyer in this case, but there is an income limit based on the AMI. This loan has a special feature where the person applying for the loan does not need to be an occupant of the home. The credit score of the applicant must be above 680.

When looking into purchasing a first home, or a subsequent one, buyers need to be aware of their financial situation, and the options available to them.

These will affect their down payment rate and mortgage loan.

There are reasonable mortgage loans that have low down payments, granted the buyer has a decent credit score.

Mortgages are essential when buying a home, and a good rate will get you the house of your dreams.

Leave A Comment