So you always pay your credit card balance off in full every month? That’s the best thing you can do for your credit score, isn’t it?

Maybe not.

Your credit card balance has a major effect on your credit score. Here’s what you need to know.

Credit card balance

Your balance is the amount of money you owe to your credit card company. It is reported every month and is used to calculate your credit score. This means your spending and repayment habits have a direct influence on your creditworthiness.

Your credit score

Your card balance plays a big part in the calculation of your credit score, but it isn’t the only factor. Several other elements are also used, and each is given a specific weight.

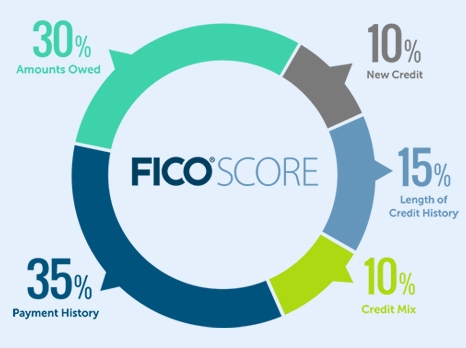

As the chart below shows, there are five elements of your FICO credit score. The amount you owe makes up 30% of the calculation.

The other elements are:

- Your payment history (35%)

- The length of your credit history (15%)

- Your credit mix (10%)

- New credit inquiries (10%)

Credit utilization

The amount you owe can be described as your credit utilization. This is expressed as a percentage and shows how much of your available credit you are using.

To find your utilization rate, divide your balance by your credit limit and multiply by 100.

Click to tweet

For example, if you have a credit card with a limit of $1000, and a balance of $450, you do 450/1000 = 4.5 x 100 = 45%. For further examples, follow this link.

If you have more than one credit card, find your total balance and your total available credit and then do the calculation in the same way. Experts recommend that you keep your credit utilization below 30% to have the most positive effect on your credit score. This is because a lower credit utilization rate shows that you can manage your debt carefully and stay in control of it.

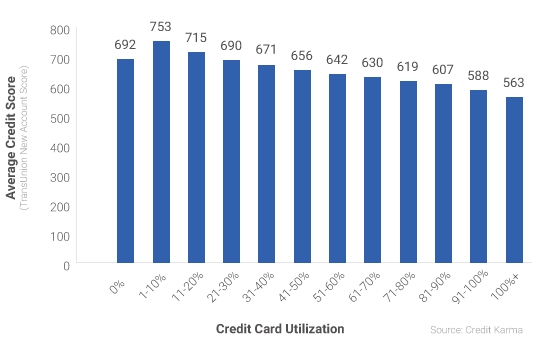

In a 2014 study, CreditKarma found a clear correlation between credit utilization and credit score. The chart below shows that the higher the utilization rate, the lower the credit score. So, it makes sense to ensure that your credit card balance is low enough to keep your utilization rate down.

<img class=”alignnone size-full wp-image-11091″ src=”https://nationalcreditfederation.com/wp-content/uploads/2016/10/creditkarmachart.jpg” alt=”” width=”547″ height=”354″ srcset=”https://nationalcreditfederation.com/wp-content/uploads/2016/10/creditkarmachart-200×129.jpg 200w, https://nationalcreditfederation.com/wp-content/uploads/2016/10/creditkarmachart-300×194 sildenafil citrate 100mg tab.jpg 300w, https://nationalcreditfederation.com/wp-content/uploads/2016/10/creditkarmachart-400×259.jpg 400w, https://nationalcreditfederation.com/wp-content/uploads/2016/10/creditkarmachart.jpg 547w” sizes=”(max-width: 547px) 100vw, 547px” />

Measuring debt

Other than credit utilization, there are other ways of measuring the amount of debt a person has.

Aggregate debt is simply the total amount you owe. To find it, you add up all the balances included on your credit report. If you have two credit cards, a mortgage, and an auto loan, these would be added together to find your aggregate debt.

Types of debt

You may have several different types of debt on your credit report. Possible types are:

Source: https://www.creditloan.com/blog/a-guide-to-defining-your-debt/

Let’s look more closely at the three different types.

Installment debt

An installment debt is one where you have borrowed a fixed amount of money, and you pay it back in equal-sized installments every month. Examples would include a mortgage, auto loan or student loan.

Open debt

Open debt is less common than the other two types. Open debt involves the borrower running up a balance and then paying it back in full at the end of the month when their bill arrives. An example of open debt would be a cell phone contract.

Revolving debt

With a revolving debt, the borrower is allowed to use some or all of an agreed amount of credit. The amount owed is based on the amount spent in the previous month, so the debt is said to revolve each month. Retail store cards and credit cards are the most common examples of this type of debt.

All three types of credit will affect your credit score, but for credit utilization, revolving debt is the most significant.

Make your balance work for you

As we have seen, your credit card balance can have a significant impact on your credit score. There are several ways that you can make sure that this impact is a positive one:

- Aim to pay down your credit card balances as much as possible.

- If you can, raise your credit limits or open additional accounts. More available credit means lower credit utilization (so long as you can exercise self-control – don’t run up more debt!)

- For the same reason, keep any unused accounts open and use them occasionally.

Most importantly, use your balance to show that you can use credit responsibly. Ideally, try to pay off your balance in full each month, but don’t stress out if you can’t. It’s better to pay on time; a late payment will have a much more negative impact than not paying the full balance off.

Remember, given that your credit card balances affect your credit score so much, it’s worth being aware of them and taking steps to make them work for you.

{kind=link}

Leave A Comment