Have you ever been denied for an auto loan, or had to pay a high interest rate on a credit card?

It may be because your credit score was not high enough. The unfortunate reality is that far too many people don’t know their credit score and the factors that come into play in determining it.

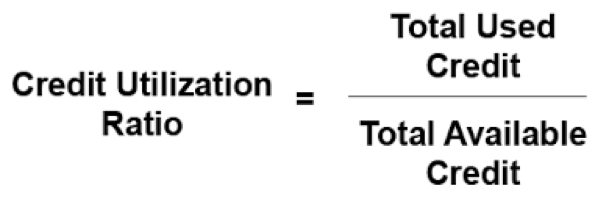

This article will cover in depth one of the most important aspects which goes into determining your credit score: your credit utilization ratio. The basic idea of the credit utilization ratio is how much of your available credit are you actually using on a regular basis?

A low credit utilization ratio means that you have a lot of available credit, but you are using a little of it.

Having a high credit utilization ratio means that you are using a large portion of the credit you have available. The ideal credit utilization ratio is approximately 33%, depending on which financial advisor you ask.

That means you should try to be using only a third of the available credit you have.

Credit cards, loans, or any other credit lines also factor into this ratio. You want to have a lot of available credit, but only use a little of it.

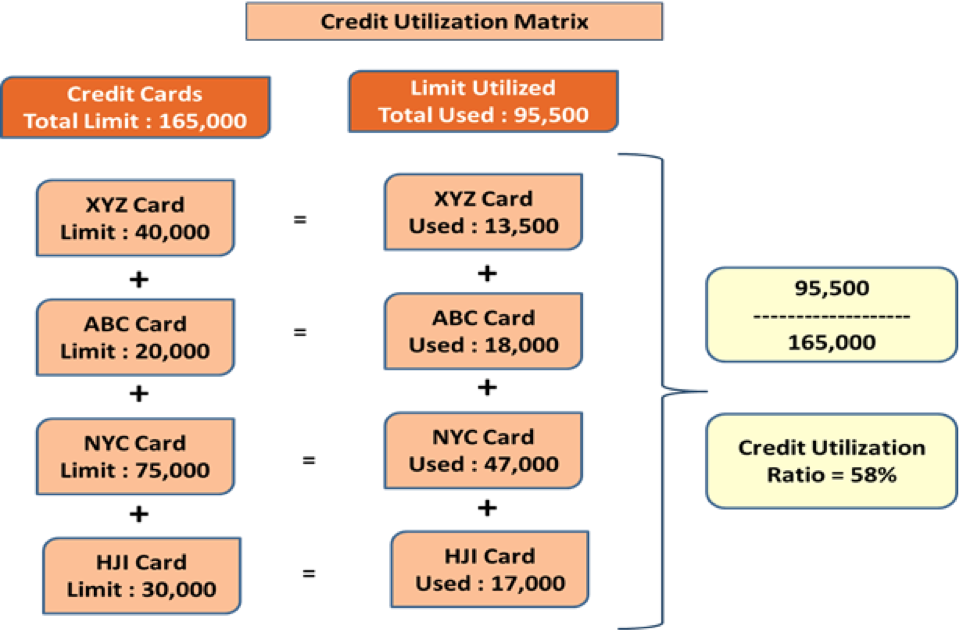

For example, say you have four credit cards with the credit limits below.

XYZ has a $40,000 limit

ABC has a $20,000 limit

NYC has a $75,000 limit

HJI has a $30,000 limit

Each of these cards’ credit limit is report as your “high credit limit” on your credit report.

Lets say you use each of these cards regularly and they have the outstanding balances listed below:

XYZ has a balance of $13,500

ABC has a balances of $18,000

NYC has a balance of $47,000

HJI has a balance of $17,000

If this were the case you’d have $95,500 in utilized credit out of a possible $165,000 available. This would you you have a total credit utilization of 58%, which is higher then the recommended amount. (Remember the highest we suggest is 30%

According to FICO, the average utilization ratio for the nation is a bit above the recommended 33%

On the other hand, say you have those same four credit cards.

But this time, the spent balance on XYZ is $6000, ABC is $5000, NYC is $7000, and HJI is $2,000.

If this were the case, you’d be utilizing $20,000 of your available $165,000 or a 12% utilization rate.

What happens when your utilization ratio goes out of whack?

It is possible that if your balance is too high on too many of your credit cards, you end up with a high credit utilization ratio. This will cause your credit score to fluctuate negatively.

You may be wondering what is considered a high utilization ratio by credit card companies and by financial advisors.

A high utilization ratio is pretty much any ratio over 1/3, or 33%. A low credit utilization ratio is ideal in terms of contributing to a high credit score. A low credit utilization ratio is considered anywhere under 1/3 for example, 20%, 15%, or 10%, which are all considered low and healthy credit utilization ratios.

A high credit utilization ratio can lower your credit score significantly over time, which is not desirable. If you have a high credit utilization ratio over a long period of time, it signifies to lenders that you may not be reliable in paying back the money that you borrowed a timely manner. Or that you do not practice responsible spending habits in general.

However, if you have a high credit utilization ratio in the short-term, it probably have a bad affect on your credit score. This is especially true if you pay off the full balance of your credit card before the end of the monthly billing cycle.

If you put a lot of money on a credit card all at once, and then pay it off before the billing cycle changes over, it should not have an effect on your credit utilization ratio at all.

The only time it can affect your credit score is if you are carrying over a balance month to month, therefore it is appearing on your monthly statements which are seen by credit reporting agencies.

Long Term affects on your credit score with a high credit utilization ratio

In general, having a high credit utilization ratio will have the biggest impact on your credit score over a longer period of time.

A high credit utilization ratio will lower your credit score consistently over time, and these impacts can add up in the long run.

Here are 11 things your credit utilization ratio can be impacted by:

- As discussed above, your credit card balance is the biggest influencing factor which goes into determining the credit utilization ratio.

- Car Loan- A car loan impacts your credit utilization ratio by increasing both the available credit and the credit being used. As you pay off the loan, you have more available credit and less being utilized, so it improves your utilization ratio. Pretty much the same concept goes for paying off any loan: it will improve your credit score.

- A mortgage is also something which can impact your credit utilization ratio. If you have a mortgage, it means that you were taking out a loan for a portion of your home. The amount of the mortgage contributes towards your available credit. As you pay it off each month, that means there’s less of the available credit being utilized. However, the available credit is still the same, thus decreasing your utilization ratio, similarly to paying off a car loan.

- You might think that student loans are a major detriment to your credit score, but so long as you’re paying off the required balance each month, paying your student loans can actually improve your credit history. Because most student loans are in such huge quantities, that vastly increases your available credit amount. That means if you’re putting a lot of money on a credit card, it has proportionally less impact than it would have if you did not have student loans.

- Business credit cards also influence credit utilization ratio. Even if the card is for business purposes, so long as it is in your name, it will be counted towards your utilization ratio.

- Credit cards with very high credit limits are usually a great influence on your credit utilization ratio. As long as you’re not using a lot of the balance on it, a high credit limit means that you have a lot of available credit. So long as you do not use a lot of it, it will help keep your credit utilization ratio very low.

- Personal loans, similar to mortgage or car loans, can have a significant and strong influence on your credit utilization ratio. If you take out a large personal loan, you’re increasing both your available credit and your credit being utilized. That means that it could sway your credit utilization ratio either way, either making it lower or higher.

- HELOCS (home equity lines) will either impact your utilization ratio positively or negatively.

- Increasing or decreasing the number of authorized users on an account or opening a joint account will also impact your utilization ratio. This is because it will increase or decrease your amount of available credit, thus changing the ratio.

- The total number of accounts with outstanding debt also has an impact.

- The total amount of debt still owed to lenders is a major portion of the ratio, similarly to your credit card balance.

All of the above factors do not have an equal impact.

Revolving credit has proportionally an 85% impact on the ratio, while installment loans proportionally only have a 15% impact.

The reason behind this is simple:

FICO doesn’t treat all different types of accounts equally. For example, a student loan and a credit card are considered very different types of debt and come into play with different impacts. Credit cards are revolving debt, and they tend to have a lot of variation in their balances.

These are the most crucial type of debt in determining the utilization ratio. In other words, keep your credit card balance low to keep your ratio low.

Having a huge student loan or mortgage doesn’t matter so much, unless you aren’t making the required regular monthly payments. It takes longer to see the benefits of making regular payments on installment loans.

In the category of amounts owed, credit card debt is much more important. It has the biggest impact on your utilization ratio.

But, it can also do the most damage to your credit score if the ratio is high, or if you don’t make timely payments.

Closing unused or unwanted credit cards can improve your credit score, even though it can increase your utilization ratio. However, be careful not to get rid of your available credit too quickly. Luckily, the ratio is not all that determines your credit score.

Here’s how credit score is determined outside of Utilization Ratio

- Payment History

- New Credit

- Length of Credit History

- Type of Credit

This concludes part 1 of 5 on how credit score is determined and why it’s so important for you, an American financial consumer, to understand this.

Leave A Comment